Discovery of the Mountain Pass deposit of rare earth metals in the USA

Foundation of the Swiss National Science Foundation

China: Export restrictions on rare earth metals

Foundation of DERA, Germany

US Executive Order 13817 on a “Federal Strategy To Ensure Secure and Reliable Supplies of Critical Minerals”

The New Geopolitical Landscape

As demand rises and supply remains concentrated, managing critical and strategic raw materials (CSRMs) has become a defining geopolitical issue. Across major economies, CSRM strategies face a shared tension: governments want secure and sustainable supply chains, but mining and processing projects are capital-intensive, slow, politically sensitive, and constrained by infrastructure and permitting bottlenecks. Countries worldwide are therefore reshaping industrial policy, trade relations, and investment strategies to secure reliable access to essential inputs for clean energy, digital infrastructure, and defence.

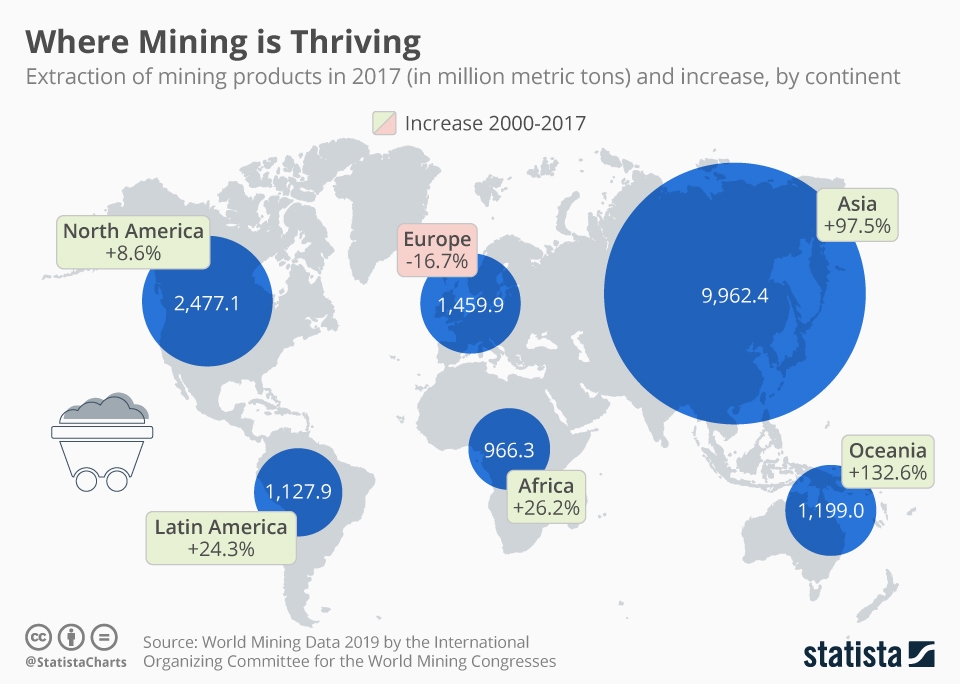

Figure 5: Europe is the only continent where mining has declined in the 21st century – despite globally rising demand. In Asia and Oceania, mining has almost/more than doubled between 2000 and 2017 [Source: Statista].

The Dominant Role of China

China frequently appears as a central risk factor for CSRM supply because of its dominant position in extraction, processing, and further manufacturing across many raw materials. This dominance emerged from decades of investment in mining and processing capacity, low production costs (sometimes due to laxer environmental and social regulation), rapid political decision-making, and strategic export policies. Most industrialised countries, by contrast, focused in the last decades on high-value downstream segments, relied on cheap imports for their manufacturing inputs. Especially in Europe, primary production eroded – creating structural dependencies.

China remains the pivotal actor in global CSRM supply chains. Its dominance is not the result of geology alone, but of decades of strategic state-backed investment in mining, refining, and midstream processing – areas many industrialised economies abandoned in favour of higher-margin segments. Combined with lower production costs, rapid regulatory decision-making, and targeted industrial policy, China now controls a decisive share of global processing for rare earths, graphite, magnesium, as well as component manufacturing such as battery materials, legacy chips, or permanent magnets. This position gives China significant leverage over international supply chains. Recent export controls on gallium, germanium, graphite, and rare earths illustrate how quickly regulatory decisions in Beijing can reshape global price dynamics, project timelines, and national risk assessments. China’s expanding overseas mining presence – particularly through Africa, Latin America, and Belt and Road investments – further extends its strategic reach. As a result, every major economy now treats diversification from Chinese-controlled midstream segments as a core strategic priority, even while remaining structurally dependent on the country’s unmatched processing capacities.

Geopolitical Leverage Through Concentration

In today’s fragmented market environment, where export restrictions, tariffs, and trade interventions often go unsanctioned, China’s concentration across key segments gives it significant leverage over global supply chains. While China clearly is the leader in most critical raw materials extraction and processing, some other countries also play important roles in individual materials due to unique geology, specialised capabilities, or historic industry development. Diversifying away from single-country dependencies has become a strategic priority for governments worldwide.

Figure 3: Countries accounting for the largest share of global CSRM production [Source: European Commission]. Note that this map does only look at either the extraction or processing stage and that the nationality of producing companies is not factored in.

Global Strategic Shifts

Here are some examples of different ways countries navigate their critical raw materials policies. The International Energy Agency keeps track of more countries’ policies.

United States: Full-Spectrum Strategic Rebuild

The United States currently approaches critical raw materials through a combined economic-security and defence lens. Its vulnerabilities stem less from geological scarcity than from decades of offshoring mining, processing, and midstream manufacturing, which have left many supply chains heavily dependent on foreign refining, particularly in China. To address these gaps, U.S. strategy increasingly targets entire value chains, aiming to expand domestic and allied capabilities in extraction, refining, material transformation, and component manufacturing for batteries, permanent magnets, semiconductors, and power electronics. Policy signals, however, although often aggressive, remain volatile. President Trump’s pauses or reversals of clean-energy incentives have created uncertainty for investors, complicating long-term planning. At the same time, targeted federal and state-level funding – including grants, loans, and tax incentives – continues to support new mining, recycling, and midstream processing capacities. The Defense Production Act (DPA) remains a central tool for accelerating strategic projects and strengthening domestic production, while U.S. agencies are simultaneously trying to expand international partnerships under U.S. leadership to diversify supply away from China.

United Kingdom: Managing High Import Dependence

Other advanced economies face very different but equally structural vulnerabilities. The United Kingdom is one of the most import-dependent high-income economies for critical raw materials; Not being a member of the EU anymore, it is acutely exposed to geopolitical shocks and trade disruptions. Decades of industrial restructuring have eroded domestic extraction and processing, while most imports enter the UK in processed form, embedded within components, electronics, and advanced materials. This makes supply-chain visibility and traceability a persistent challenge. UK strategy therefore centres on diversification, circularity, and intelligence-building rather than large-scale domestic mining. Current efforts prioritise strengthening recycling and remanufacturing capabilities, improving data and early-warning systems through the Critical Minerals Intelligence Centre (CMIC), and expanding partnerships with trusted suppliers. Given limited geological potential, the UK focuses on niche capacities – such as specialised magnet recycling or tungsten processing – where small-scale, high-value production can strengthen resilience without requiring large upstream industries.

Japan: Economic Security Through Long-Term Partnerships

Japan integrates critical raw materials deeply into its broader economic security doctrine, shaped by its acute import dependence and the lasting impact of the 2010 rare-earth crisis. The country’s resilience strategy combines diversified overseas investments, national stockpiling, and close state-industry coordination through institutions such as the Japan Organization for Metals and Energy Security (JOGMEC), which actively supports exploration, project financing, joint purchasing, and midstream processing capacity. Japan’s approach emphasises long-term relationships with partner countries – such as Australia –, often backed by public guarantees and co-investment structures designed to reduce private-sector risk. Recent policies (METI: Japan’s new international resource strategy to secure rare metals (2020)., JOGMEG Critical Minerals Subsidy Program (2023, in Japanese), METI Policy on initiatives for ensuring stable supply of critical minerals (2022, in Japanese)) place renewed focus on securing stable supplies for GX (Green Transformation) and DX (Digital Transformation) technologies, including batteries, motors, semiconductors, and hydrogen systems. Alongside upstream investments, Japan is expanding efforts in recycling, substitution R&D, and traceability initiatives to improve supply-chain transparency. The result is a system in which the government plays a hands-on role in steering industrial strategy, ensuring that Japan’s globally competitive manufacturing sectors retain access to the materials they rely on.

The EU’s Response

Europe’s Structural Dependence on Imports

The EU is one of the world’s most import-dependent regions for critical raw materials, particularly for those processed in China. Having invested in segments that promised higher value creation and with increasing globalization and cheap imports, the mining sector has steadily declined in the last decades.

The Critical Raw Materials Act: Strategic Autonomy in Practice

The EU focuses strongly on reducing import dependence and building strategic autonomy through the Critical Raw Materials Act (CRMA), in force since 2024. Benchmarks to be reached by 2030 aim to expand extraction, processing, recycling, and diversification for raw materials deemed strategic for the European Union. Yet the EU faces slow permitting, complex ESG expectations, and competition for investments from regions with faster project development and large subsidies. Europe’s strategy relies heavily on international partnerships to secure sustainable supplies while developing midstream capacity at home.

Figure 6: Benchmarks for EU strategic raw materials, to be reached by 2030 [Source: European Commission].

Strategic Projects: Fast-Track Tools for Key Value Chains

Under the CRMA, the EU designates certain mining, processing, recycling, and substitution projects as strategic projects. These projects must deliver a meaningful contribution to European supply, meet strict ESG criteria, and qualify under accelerated permitting rules. In return, they benefit from accelerated permitting timelines, coordinated access to financing, and recognition as priority infrastructure, helping reduce investment risk and shorten time-to-market – a critical factor in CSRM value chains where project development typically spans more than a decade. However, so far there is no direct funding for strategic projects available.

ReSourceEU: Strengthening EU Governance and Preparedness

To operationalise CRMA implementation, the European Commission adopted the RESourceEU Action Plan in early 2025. This initiative shall strengthen CRMA governance and monitoring capacities through measures such as:

- enhanced tracking of strategic dependencies across the entire value chain,

- mechanisms for earlier detection of supply risks, enabling coordinated EU-level responses,

- improved and accelerated access to finance, by de-risking investments and steering capital toward strategic CRM projects,

- the creation of an EU Critical Raw Materials Centre to coordinate stockpiling and joint purchasing – Japan’s JOGMEC is mentioned as a role model.

The EU’s response to CSRM risks in a rapidly shifting global environment reflects a balancing act between market openness, democratic decision‑making, and the need for speed. Its success will rest on whether this equilibrium can translate ambitious policy into timely, well‑financed action amid intensifying global competition for critical raw materials.